Debt Management

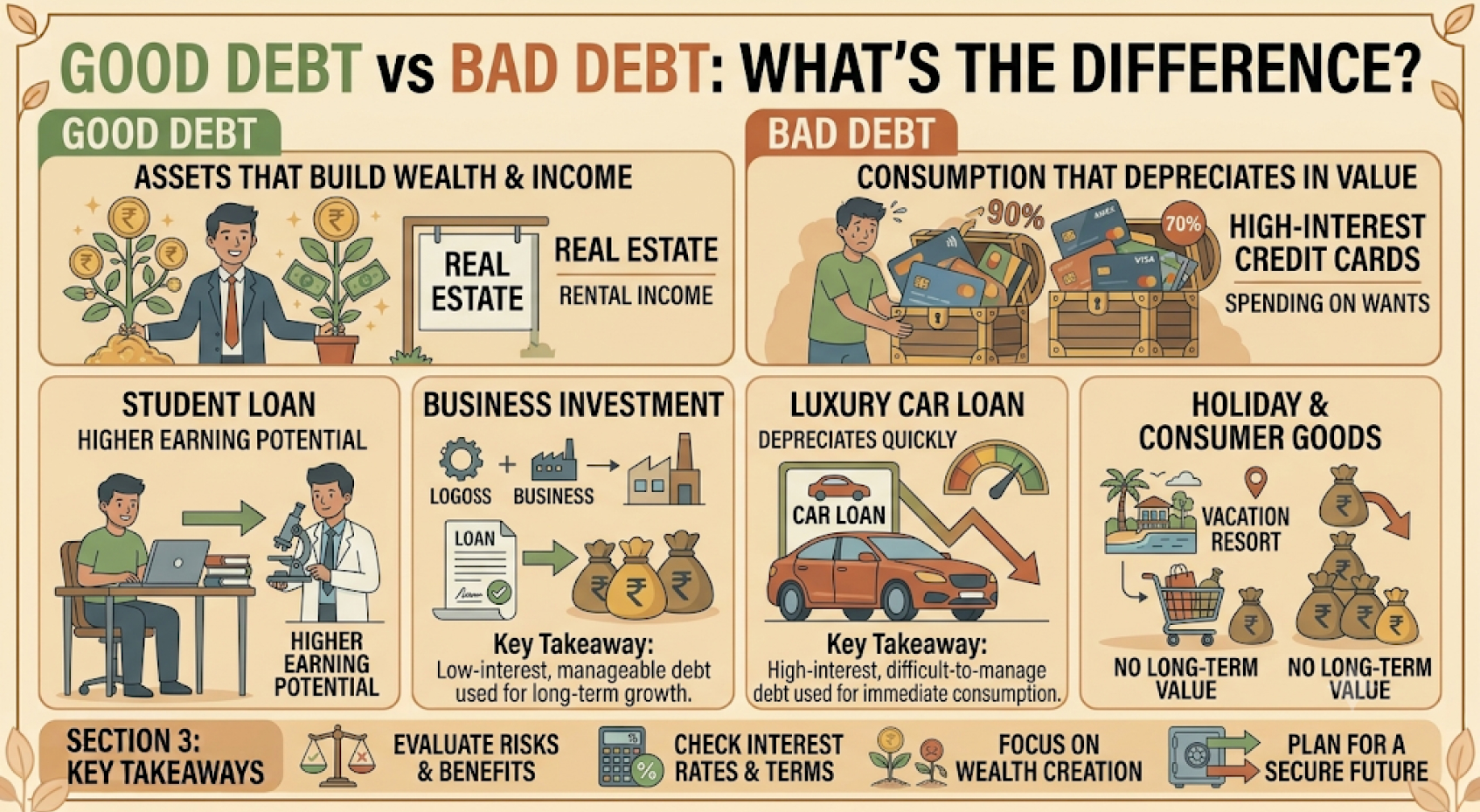

Good Debt vs Bad Debt: What's the Difference?

Not all debt is harmful. Some types of borrowing can help you build wealth or increase your future earning potential, while others may create financial stress and make it harder to reach your goals. Understanding the difference between good debt and bad debt helps you borrow more responsibly.

The purpose of the debt, its cost, and your ability to repay it are the key factors that determine whether borrowing is beneficial or harmful.

What Is Good Debt?

Good debt is money borrowed to purchase something that is likely to increase in value or improve your financial future. When managed responsibly, this type of debt can provide long-term benefits.

Examples of Good Debt

- Student loans that improve career opportunities.

- Home loans used to purchase property.

- Business loans that help grow a profitable business.

- Loans for essential home improvements that increase property value.

What Is Bad Debt?

Bad debt is borrowing money for items that quickly lose value or for purchases you cannot comfortably afford. High-interest debt can become difficult to repay and reduce your ability to save or invest.

Examples of Bad Debt

- High-interest credit card balances that are not paid off.

- Loans for unnecessary luxury purchases.

- Payday loans with extremely high interest rates.

- Borrowing to support excessive lifestyle spending.

How to Borrow Wisely

- Borrow only when necessary.

- Compare interest rates before taking a loan.

- Ensure monthly payments fit your budget.

- Avoid borrowing for non-essential purchases.

- Pay loans on time to protect your credit history.

- Reduce high-interest debt as quickly as possible.

Signs Your Debt May Be Becoming a Problem

If you're relying on credit to pay everyday expenses, missing loan payments, carrying large credit card balances, or borrowing money to repay existing debt, it may be time to review your financial situation and create a repayment plan.

Benefits of Using Debt Responsibly

Responsible borrowing can help build a positive credit history, finance valuable assets, support education or business growth, and improve long-term financial opportunities without creating unnecessary financial stress.

FAQs

Is all debt bad?

No. Some debt, such as education or home loans, can provide long-term financial benefits when managed responsibly.

Why are credit card balances often considered bad debt?

High-interest credit card debt can become expensive if balances are carried for long periods, making it difficult to repay.

Can good debt become bad debt?

Yes. Even beneficial loans can become problematic if payments are missed or the debt becomes unaffordable.

How can I avoid bad debt?

Create a budget, borrow only when necessary, compare loan options, and make all payments on time.